All Categories

Featured

Table of Contents

The essential difference between typical UL, Indexed UL and Variable UL lies in exactly how cash money value build-up is computed. In a typical UL policy, the money value is assured to grow at a rates of interest based on either the present market or a minimum rates of interest, whichever is greater. So, for example, in a conventional Guardian UL plan, the yearly rates of interest will certainly never ever go lower than the present minimum price, 2%, but it can go higher.

In a negative year, the subaccount value can and will certainly reduce. These policies allow you designate all or component of your cash worth growth to the efficiency of a broad protections index such as the S&P 500 Index. 7 Nevertheless, unlike VUL, your cash is not really purchased the market the index simply provides a referral for exactly how much interest the insurance coverage credits to your account, with a flooring and a cap for the minimum and optimum prices of return.

Most plans have annual caps, but some policies might have monthly caps. Furthermore, upside efficiency can be influenced by a "participation price" established as a percentage of the index's gain.

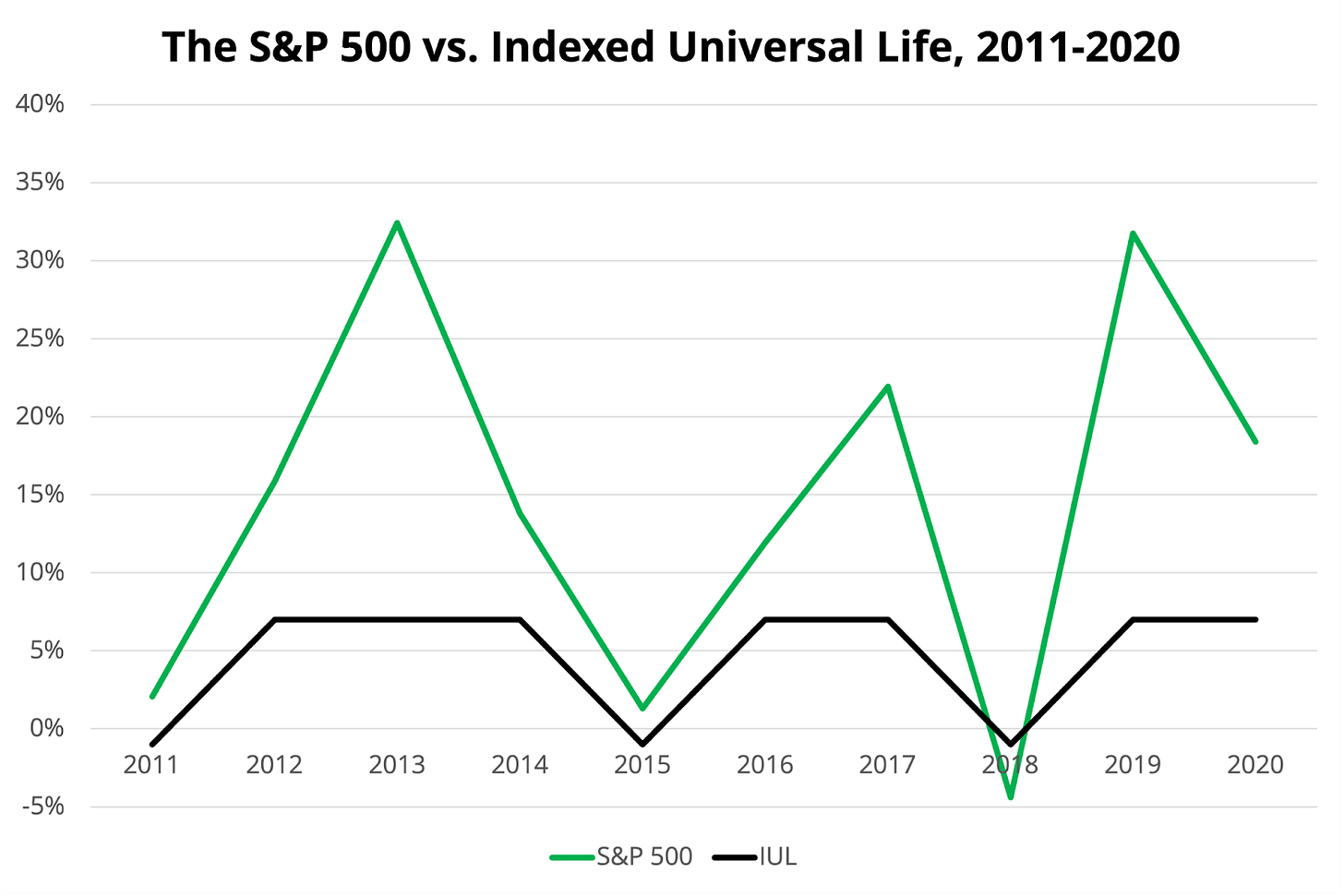

Most Indexed UL plans have an involvement rate set at 100% (significance you understand all gains up to the cap), but that can transform. Presuming you made no changes to your allocation, below's what would have taken place the next year: 80% S&P 500 Index$8,000 +24.2%100%11%11%$880$8,88020% Fixed-rate$2,060 NANA3%$62$2,122 Over this abnormally unpredictable two-year span, your ordinary cash money value growth price would have been close to 5%.

Like all various other kinds of life insurance, the key purpose of an indexed UL policy is to give the economic protection of a death advantage if the insurance policy holder dies all of a sudden. Having claimed that, indexed UL policies can be specifically attractive for high-income individuals who have maxed out various other pension.

Universal Life Insurance Cash Value Withdrawal

There are additionally important tax ramifications that insurance holders ought to be aware of. For one, if the plan lapses or is surrendered with an outstanding financing, the loan quantity might become taxed. You should likewise find out about the "Internal Revenue Service 7-Pay Examination": If the advancing premiums paid during the first seven years go beyond the amount needed to have the plan compensated in 7 degree yearly repayments, the plan comes to be a Modified Endowment Agreement (or MEC).

So it is very important to speak with a monetary or tax expert that can aid ensure you make the most of the advantages of your IUL plan while staying compliant with internal revenue service policies. Because indexed UL plans are rather complex, there have a tendency to be higher management costs and expenses compared to various other forms of long-term life insurance coverage such as entire life.

This advertising widget is powered by, a certified insurance coverage producer (NPN: 8781838) and a company affiliate of Bankrate. The offers and clickable links that show up on this ad are from business that compensate Homeinsurance.com LLC in various methods. The compensation obtained and various other variables, such as your area, might influence what ads and links appear, and how, where, and in what order they appear.

We make every effort to maintain our details exact and up-to-date, but some details may not be present. Your real deal terms from an advertiser may be different than the offer terms on this widget. All deals may undergo added terms and conditions of the advertiser.

When intending for the future, you wish to try to provide yourself the ideal feasible possibility for assurance, and economic safety for you and your liked ones. This normally calls for some mix of insurance coverage and financial investments that have excellent growth potential over the longer term. What if we told you there was a life insurance alternative that integrates peace of mind for your loved ones when you pass along with the opportunity to produce extra profits based on particular index account performance? Indexed Universal Life Insurance policy, commonly abbreviated as IUL or described as IUL insurance coverage, is a vibrant blend of life protection and a money worth element that can expand depending on the efficiency of popular market indexes.

Find out extra about just how an IUL account features, how it compares to ensured global life insurance policy, some pros and cons, and what policyholders require to understand. IUL insurance is a kind of irreversible life insurance policy. It not only ensures a survivor benefit, but has a money value component. The specifying characteristic of an IUL policy is its growth potential, as it's tied to details index accounts.

Life Insurance Stock Index

Survivor benefit: A hallmark of all life insurance policy products, IUL plans additionally promise a survivor benefit for beneficiaries while coverage is active. Tax-deferred development: Gains in an IUL account are tax-deferred, so there are no prompt tax obligation responsibilities on gathering earnings. Finance and withdrawal alternatives: While available, any type of financial communications with the IUL policy's cash value, like loans or withdrawals, need to be approached sensibly to avoid diminishing the death benefit or sustaining taxes.

They're structured to make sure the policy continues to be active for the insured's life time. Comprehending the benefits and drawbacks is pivotal before selecting an IUL insurance coverage strategy. Development capacity: Being market-linked, IUL policies might generate much better returns than fixed-rate financial investments. Guard against market slides: With the index features within the item, your IUL policy can remain protected against market drops.

appeared January 1, 2023 and offers assured acceptance whole life insurance coverage of up to $40,000 to Experts with service-connected impairments. Discover more about VALife. Lesser amounts are readily available in increments of $10,000. Under this strategy, the chosen protection works two years after registration as long as costs are paid during the two-year period.

Protection can be expanded for up to two years if the Servicemember is totally disabled at separation. SGLI coverage is automatic for most active service Servicemembers, Ready Reserve and National Guard participants arranged to perform at least 12 periods of inactive training per year, members of the Commissioned Corps of the National Oceanic and Atmospheric Administration and the general public Health Service, cadets and midshipmen of the U.S.

VMLI is offered to Experts who received a Specifically Adapted Housing Give (SAH), have title to the home, and have a home mortgage on the home. closed to brand-new registration after December 31, 2022. We began approving applications for VALife on January 1, 2023. SGLI protection is automated. All Servicemembers with permanent insurance coverage should make use of the SGLI Online Enrollment System (SOES) to mark beneficiaries, or reduce, decrease or bring back SGLI insurance coverage.

Term Life Insurance Vs Universal Life Insurance

All Servicemembers ought to use SOES to decrease, reduce, or restore FSGLI protection.

After the very first plan year, you might take one annual, free partial withdrawal of as much as 10% of the total build-up value without surrender costs. If you withdraw greater than 10% of the accumulation worth, the cost applies to the amount that goes beyond 10%. If you make greater than one partial withdrawal in a policy year, the fee applies to the amount of second and later withdrawals.

The remaining money can be purchased accounts that are connected to the efficiency of a securities market index. Your principal is ensured, but the quantity you gain undergoes caps. Financial planners typically recommend that you first max out various other retired life savings options, such as 401(k)s and Individual retirement accounts, prior to taking into consideration investing via a life insurance policy plan.

{kind=link}

Table of Contents

Latest Posts

Index Universal Life Insurance Companies

Iul Insurance Meaning

Iul For Dummies

More

Latest Posts

Index Universal Life Insurance Companies

Iul Insurance Meaning

Iul For Dummies